Understanding Credit Consolidation in Canada

Credit consolidation is an essential financial strategy for many Canadians grappling with overwhelming debt. It serves as a viable solution to combine various debts into a single monthly payment, helping individuals regain control over their finances. When exploring options, https://credit-consolidation.ca/ provides comprehensive insights into how to navigate this process effectively. This article delves into what credit consolidation entails, the myriad benefits it offers, and addresses common misconceptions that often hinder individuals from seeking help.

What Is Credit Consolidation?

Credit consolidation refers to the process of merging multiple debts into a single loan or payment plan. This approach is primarily aimed at simplifying repayment and can encompass various types of unsecured debts, including credit card bills, personal loans, and medical expenses. By consolidating debts, individuals typically enjoy lower interest rates, reduced monthly payments, and a clearer path towards debt elimination.

Benefits of Credit Consolidation

The benefits of credit consolidation are numerous, particularly for those overwhelmed by multiple debt obligations. Some primary advantages include:

- Lower Monthly Payments: By consolidating debts, individuals can significantly reduce their monthly financial burden, allowing for better cash flow management.

- Reduced Interest Rates: Many consolidation options provide the opportunity to secure a lower interest rate, which decreases the overall cost of repaying the debt.

- Simplified Payments: Instead of managing several payments each month, consolidation allows for a single payment, making financial management easier.

- Improved Credit Score: Successfully managing a consolidated debt can enhance an individual's credit score over time, improving access to future financial products.

Common Misconceptions Explained

Despite its benefits, several misconceptions about credit consolidation often deter individuals from pursuing this solution. One common myth is that consolidation is the same as debt settlement. While both aim to alleviate debt, consolidation combines debts into one payment, whereas settlement involves negotiating to pay less than what is owed. Additionally, many people fear that entering a consolidation program will harm their credit score; however, responsibly managing a consolidation loan can actually improve an individual's credit rating in the long run.

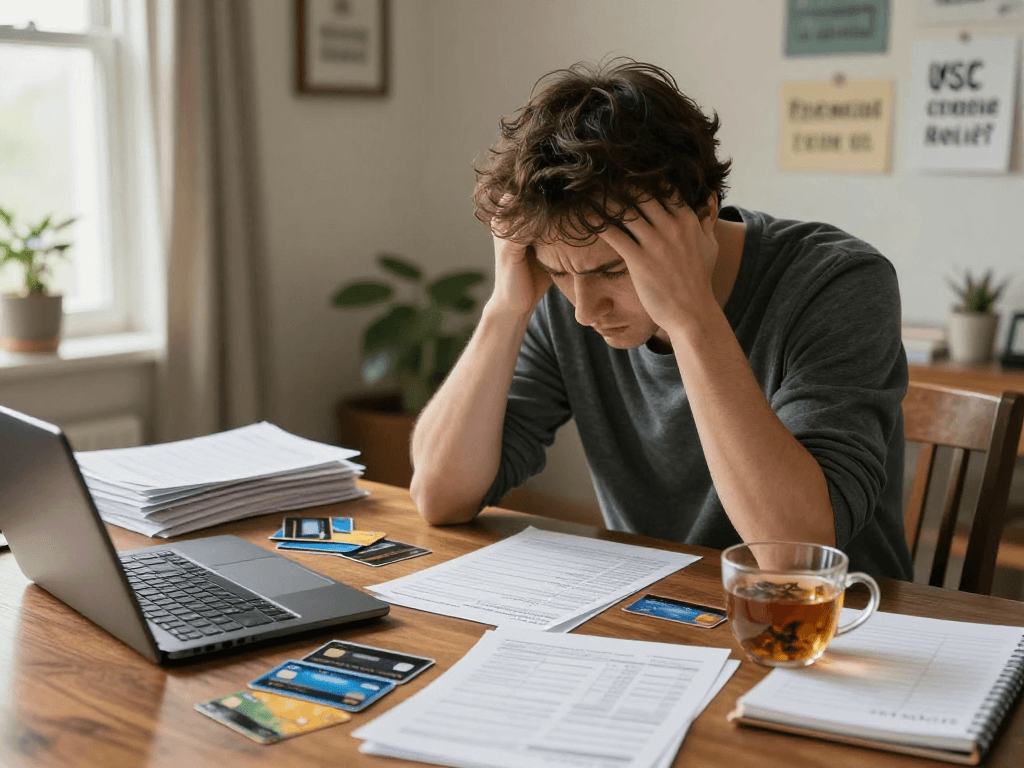

Challenges Faced by Canadians with Unsecured Debts

For many Canadians, unsecured debt can feel like an insurmountable challenge. Understanding the landscape of these debts is crucial for those seeking relief. Unsecured debts, unlike secured debts such as mortgages, are not backed by collateral, leaving individuals vulnerable to collection practices and financial instability.

The Debt Trap: Statistics You Should Know

Recent statistics reveal that the average Canadian household carries approximately $7,194 in credit card debt. With rising costs of living and stagnating wages, many individuals find themselves caught in a cycle of borrowing to meet monthly obligations. This trend extends beyond the immediate financial implications and often leads to broader economic impacts, including decreased consumer spending and increased reliance on credit.

Impact of Unsecured Debts on Mental Health

The burden of unsecured debts not only poses financial challenges but also takes a significant toll on mental health. Many Canadians report feelings of anxiety, distress, and even depression as a result of their financial struggles. The constant worry about payments, creditor calls, and the potential for bankruptcy can create a pervasive sense of hopelessness. Seeking help through credit consolidation can be a pivotal step in alleviating this stress.

How to Identify Your Debt Levels

To effectively tackle unsecured debts, it is essential to first assess and understand one's financial situation. Here are some steps to consider:

- Create a Comprehensive List: Document every debt, including creditor names, outstanding balances, and interest rates.

- Calculate Monthly Payments: Determine how much you are currently paying each month towards your debts to understand your financial outflow.

- Review Your Budget: Analyze your income versus expenses to identify areas where you can cut back and allocate funds towards debt repayment.

Effective Credit Consolidation Solutions for Canadians

With a clear understanding of their financial situation, Canadians can explore various credit consolidation solutions tailored to their needs. Each option offers different benefits and is suited to different circumstances.

How to Choose the Right Consolidation Plan

Choosing the right consolidation plan involves considering several factors, such as the types of debt, the total amount owed, and individual financial goals. Options include personal loans, home equity loans, and credit counseling services. It is essential to compare interest rates, terms, and fees associated with each option before making a decision.

Role of Credit Counseling Services

Credit counseling services play a critical role in helping Canadians manage their debts effectively. These organizations provide resources, education, and support to individuals seeking to improve their financial health. A certified credit counselor will assess your financial situation and recommend tailored strategies, including debt management plans (DMPs) that can facilitate the consolidation process.

Negotiating with Creditors

Another critical step in the credit consolidation process is negotiating with creditors. During this phase, a credit counselor can advocate on your behalf, discussing potential payment reductions, interest rate adjustments, and waiving of fees. Many creditors prefer to negotiate rather than risk a debtor defaulting on their loans, making it a valuable step in achieving favorable repayment terms.

Steps to a Successful Debt Consolidation Journey

Embarking on a debt consolidation journey may seem daunting, but breaking it down into manageable steps can facilitate a more effective process.

The Initial Consultation Process

The first step in debt consolidation is typically an initial consultation with a credit counselor. During this meeting, you will discuss your financial situation, including debts, income, and expenses. This information helps the counselor develop a personalized debt management strategy designed to suit your unique needs.

Creating a Sustainable Budget Post-Consolidation

Once a consolidation plan is established, it's crucial to create a sustainable budget that prioritizes debt repayment. This budget should take into account all monthly expenses, savings goals, and debt payments, ensuring that individuals remain on track to achieve financial freedom.

Tracking Your Progress and Success

Monitoring your progress is vital in your journey towards financial stability. Regularly reviewing your budget, tracking payments, and assessing changes in your credit score can provide motivation and accountability as you work toward eliminating your debt.

Looking Ahead: The Future of Credit in Canada

As the financial landscape continues to evolve, Canadians must stay informed about emerging trends in debt management and credit consolidation. The ability to adapt to these changes will be key to achieving long-term financial health.

Emerging Trends in Debt Management for 2026

Looking ahead to 2026, several trends are poised to shape debt management strategies. These include increased reliance on digital tools for budgeting and debt tracking, a growing emphasis on financial literacy education, and the rise of personalized financial services tailored to individual needs.

How Technology is Transforming Credit Solutions

Technology is revolutionizing the way Canadians approach credit solutions. Online platforms offer immediate access to credit counseling services, allowing individuals to seek help from the comfort of their homes. Additionally, tools such as budgeting apps and financial tracking software simplify the management of personal finances.

Preparing for Financial Independence

Ultimately, the goal of credit consolidation and debt management is to achieve financial independence. By understanding their debt levels, utilizing effective consolidation strategies, and making informed financial decisions, Canadians can pave the way toward a more secure financial future.

What are the first steps in credit consolidation?

The first steps generally include assessing your current debt, creating a list of your creditors, and reaching out to a credit counseling service for guidance.

How can I choose a reliable credit counseling service?

To select a reliable credit counseling service, look for accreditation from recognized agencies, read client reviews, and ensure they offer free initial consultations.

What should I know before consolidating my debts?

Before consolidating, understand the terms of the consolidation plan, including fees, interest rates, and the impact on your credit score.

How long does the credit consolidation process take?

The duration of the credit consolidation process varies, but it typically ranges from a few weeks to several months, depending on individual circumstances and the complexity of the debts involved.

Will credit consolidation improve my credit score?

Yes, responsibly managing your consolidated debt can lead to improvements in your credit score over time as you demonstrate consistent payments and reduce your overall debt load.